Reading indicators signal further weakening in Russia’s industrial economy. Forward-looking and survey data point to a continued deterioration in Russia’s industrial sector and broader economy. Industrial demand has fallen to a post-pandemic low, while sales expectations have slipped back to their weakest levels since March 2022. Borrowing conditions for manufacturers have tightened to levels last seen during the 2008–2009 crisis. The Central Bank maintains that the economy is emerging from overheating. Economists, however, argue that the civilian sector is already nearing conditions comparable to the 2008–2009 downturn, pointing to a broad-based slowdown.

Rail freight volumes, a key proxy for economic activity, reinforce the picture. Russian Railways (RZD) said on Thursday that March loading fell 2.1 % year on year to 95.6 million tonnes. Compared with March 2024, volumes were down 9 %, and nearly 16 % lower than in 2019.

Total loading for January to March 2026 reached 269.1 million tonnes, down 3.1 % from the same period last year, according to preliminary data. Declines were recorded across coal, coke, oil, pipes, ferrous metals, construction materials and industrial inputs.

‘The main drag on overall loading comes from weaker bulk shipments, reflecting declining activity in sectors such as coal, metals and construction,’ the company said.

The Institute of Economic Forecasting of the Russian Academy of Sciences (IEF RAS) said the optimism seen at the end of 2025 faded in the first quarter of 2026. Demand expectations in March fell to their lowest level since March 2022. Industrial firms now expect the weakest sales performance since the start of the military campaign in the second quarter, according to IEF RAS economist Sergei Tsukhlo.

Industrial output deteriorated sharply in March, according to surveys of manufacturers. The balance of actual output changes fell close to its weakest post-pandemic level, last seen in September 2025. Output plans, which had strengthened in December and January, slid in March to their lowest since March 2022.

Dissatisfaction with the use of machinery and equipment hit a record high in March, according to Sergei Tsukhlo.

‘The policy-driven cooling of the economy has produced the worst pattern of capacity utilisation assessments in the entire 2014–2026 monitoring period. In the first quarter of 2026, the share of normal assessments fell to 36 %, an all-time low and half the peak recorded in the third quarter of 2023,’ he said.

Tsukhlo noted that satisfaction with capacity utilisation began to decline after the second quarter of 2024, when 70 % of industrial companies reported normal levels.

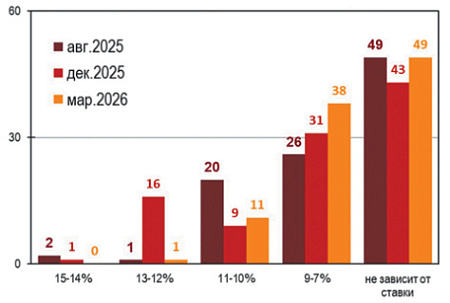

IEF RAS also says Russian companies have revised their view of the key rate needed to trigger sustained growth in output, investment and borrowing. Firms now say they would start expanding production only if the key rate falls to 11–10 %, compared with 13–12 % last year.

Limited access to credit remains one of industry’s biggest problems. In the first quarter, companies rated credit availability at its worst level since the 2008–2009 crisis. Only a third of firms consider current lending conditions normal. According to the institute, companies would begin borrowing at a key rate of 11–10 %, while lending would become broad-based only if the rate fell to 9–7 %.

Investment plans show a similar pattern. Russian industry now says it would begin investing at a key rate of 11–10 %, though most companies are waiting for a fall to 9–7 %. At the same time, overall satisfaction with actual investment volumes in the first quarter dropped to the lowest point in the entire 2010–2026 monitoring period, Tsukhlo said. Only 37 % of companies described their investment levels at the start of this year as normal. Two years earlier, by contrast, almost 80 % said their investment volumes were sufficient.

Russian manufacturers also reported a further deterioration in operating conditions in March, according to S&P Global. The manufacturing purchasing managers’ index fell to 48.3 in March 2026 from 49.5 a month earlier. A reading above 50 signals growth in business activity, while one below 50 points to contraction.

Analysts said the downturn gathered pace as output and new orders fell more quickly amid weaker demand. Lower production needs also led to the sharpest cut in raw material purchases since March 2022, while companies reduced both headcount and inventories. Business confidence fell to its lowest level in nearly four years, reflecting concern about consumers’ purchasing power.

An increasing number of sectors in Russia’s economy are sliding into recession or a severe downturn, says financial analyst Pavel Ryabov, who runs the Telegram channel Spydell_finance.

‘The economy is splitting into clearly distressed industries, segments stuck in stagnation and those still expanding. However, growth is almost entirely concentrated in sectors driven by state demand when weighted by revenue. Strip that out, and the decline exceeds the 2015–2016 downturn, with the cumulative impact now comparable to 2009,’ he said.

‘Civilian output is in its deepest crisis since 2009, wiping out the gains of 2023–2024 and falling back to 2016–2021 levels. Manufacturing is still being propped up by the defence sector, though even that is losing momentum,’ he added.

Manufacturing is now contracting at its fastest pace since 2022. At the peak of that crisis, output fell by 3.2 %; current declines stand at 2.8–3 %. Seventeen manufacturing industries, accounting for 71.8 % of sector revenue, are in decline, dragging the sector down by 2.8 % year on year in February, according to Ryabov. Only seven industries, representing 28.2 %, are still growing.

Overall industrial output continues to shrink at its fastest rate since 2022. Production fell 0.9 % year on year in February, after a 0.8 % drop in January. Comparable weakness was last seen in early 2023, while sustained contraction was previously observed in 2022, Ryabov noted.

The broader economy is following a similar path. Output of goods and services in core sectors fell 2.44 % year on year in February, after a 3.2 % drop in January.

‘Over the first two months, the decline reached 2.8 %, broadly in line with the weakest periods of 2022 and 2015, but this includes the positive effect of state-driven growth segments,’ he said.

‘Industrial activity is characterised by prolonged stagnation that has tipped into outright decline since early 2026. Demand, output and employment indicators have fallen to levels seen during the crises of 2020 and 2022, while some metrics, including investment satisfaction and credit availability, are now comparable to the 2008–2009 crisis,’ said Anastasia Levchenko, a researcher at the Gaidar Institute.

Russia’s Central Bank says the economy is close to closing its output gap, signalling an earlier-than-expected exit from overheating. The assessment was outlined in a summary of the Central Bank’s March 20 key rate meeting. ‘Preliminary data show growth slowed markedly in the first quarter of 2026,’ the Central Bank said, adding that activity has been more subdued than it had forecast in February. While the output gap remains slightly positive, it is narrowing.

The Central Bank says the economy is close to closing its output gap, though it remains slightly positive. ‘Weaker domestic demand than expected suggests the gap may close faster than projected in February,’ the regulator said. In its February outlook, the Central Bank expected the positive output gap, under tight monetary conditions, to close in the first half of 2026.

The Central Bank also pointed to ‘room to cut the key rate’. ‘The easing of domestic demand overheating is happening faster than expected. Holding the rate at current levels risks overcooling the economy and a significant undershoot of the inflation target,’ it warned.

Vladimir Chernov, an analyst at Freedom Finance Global, said March data indicate industry is entering a cooling phase.

‘Tight monetary policy, weak domestic demand and the lagged impact of high borrowing costs are now weighing on output and investment. As debt builds, servicing costs rise, adding further pressure. External uncertainty is also holding back activity,’ he said. As a result, the economy is slowing, with industry, as the most cycle-sensitive sector, reacting first,’ he said.

In effect, the economy is moving from the overheated conditions of 2023–2024 into a hard landing outside the state sector, said Yaroslav Kabakov, strategy director at Finam. In his view, this is no longer just a correction, but not yet a full-blown crisis, with stagnation taking hold and risks of further deterioration.

‘Pressure is coming from several fronts: high borrowing costs, a fading fiscal impulse, weaker consumption and a structural tilt towards defence that is crowding out civilian investment,’ he said.

‘New orders are falling at the fastest pace since October 2025, output is declining, companies are cutting raw material purchases amid weak demand and high rates, and firms see little reason to expand capacity. All of this points to a sharp deterioration in industrial conditions in March 2026,’ said Dmitry Baranov, a senior analyst at Finam Management.

Kabakov expects industry in 2026 to hover around zero growth or slip slightly into contraction, while the broader economy is likely to post only marginal expansion.

‘On the one hand, the slowdown is not unexpected. The cooling in business activity has been evident since early 2025 and is directly linked to high interest rates weighing on manufacturing. A strong rouble and relatively low oil prices have added pressure on the oil and gas sector, with the slowdown spilling over into related industries such as drilling. On the other hand, a recession driven by tight monetary policy, while military operations continue abroad, looks highly contradictory. If it escalates into a full-scale financial and economic crisis, it would not only carry reputational costs but could also be seen as a defeat in an economic confrontation, undermining confidence in the rouble. That, in turn, would weaken the currency and trigger a surge in inflation. In such a scenario, serious questions would arise over whether monetary policy is appropriate to current conditions,’ said Vladimir Bragin, head of financial markets and macroeconomic analysis at Alfa-Capital.