Three key agencies, the Central Bank, the Ministry of Finance and the Ministry of Economic Development, will discuss at SPIEF how to coordinate monetary, fiscal, tax and broader economic policy in order to put the country back on a path of sustainable growth. Forum organisers, clearly anticipating a discussion with far-reaching implications, have already begun shaping the debate. Roscongress has published a report calling for a ‘serious restructuring’ of both the economic model and monetary policy.

This year’s forum will be a test for the Central Bank. Elvira Nabiullina’s institution will have to defend its decisions in a situation where it appears that almost everyone is against it: lawmakers, businesses, economists and even the organisers of the forum themselves.

Roscongress set the tone in advance by publishing a report titled ‘The Growth Potential of the Russian Economy. Returning to a Development Trajectory: From Changes in Monetary Policy to a New Model’. The title itself implies that changes in the Central Bank’s approach are taken as a given.

On the very first page, the authors laid out their main arguments:

‘The stated goals of current monetary policy limit the economy’s growth potential. Inflation remains structurally above the 4% target because of supply constraints. Falling profitability below the cost of funding has reinforced the trend toward lower investment. A strong rouble under the current model does not help import substitution. Recalibrating monetary policy and synchronising it with fiscal and industrial policy would help support the economy.’

The report notes that Russia’s economy showed strong growth rates from the early 2000s. More modest growth began in the mid-2010s, coinciding with the introduction of inflation targeting, under which the Central Bank sets itself an inflation goal and seeks to achieve it through policy measures.

But measures that could previously be justified have been facing increasing criticism since 2022.

‘The Central Bank’s logic is understandable,’ the report says. ‘Its mandate requires defeating inflation at any cost. Yet it can effectively influence only the market component of demand. Inflation in Russia has long had a non-monetary nature. The core problem is rising costs, which producers pass on through prices while output declines.’

‘Given the West’s efforts to wear down the Russian economy, it is obvious that current realities require specialised measures and a serious restructuring of both the economic model in general and monetary policy in particular,’ the authors wrote, adding that policymakers should finally recognise ‘the fact that reducing inflation and keeping it near the 4% target is unlikely under current structural conditions’.

Instead, they argue that what is needed is ‘close interaction between the Central Bank and the government in achieving both inflation and sustainable growth targets’. ‘The new economic realities require a dual mandate of economic growth and price stability,’ the report says.

Among the recommendations is a shift to a more stimulative policy aimed at expanding investment and production activity, as well as a lower real interest-rate regime, ‘closer to 2–4% rather than the current 9–10%’. The report defines the real rate as the Central Bank’s key rate adjusted for inflation.

At the same time, the authors propose maintaining strict macroprudential controls to prevent a repeat of the ‘inefficient credit boom’ of 2023–2024.

‘This implies a gradual rollback of subsidised lending programmes financed through the budget,’ they wrote.

Another proposal emerging from the Roscongress discussions was that lending to ‘strategic budget sectors’ such as the special military operation, the military-industrial complex and other state-funded enterprises ‘should be removed from the Central Bank’s perimeter’. Instead, their development should be supported through a special agency and refinancing instruments. Inflation generated by their activity, the report says, should be excluded from the country’s overall consumer price index.

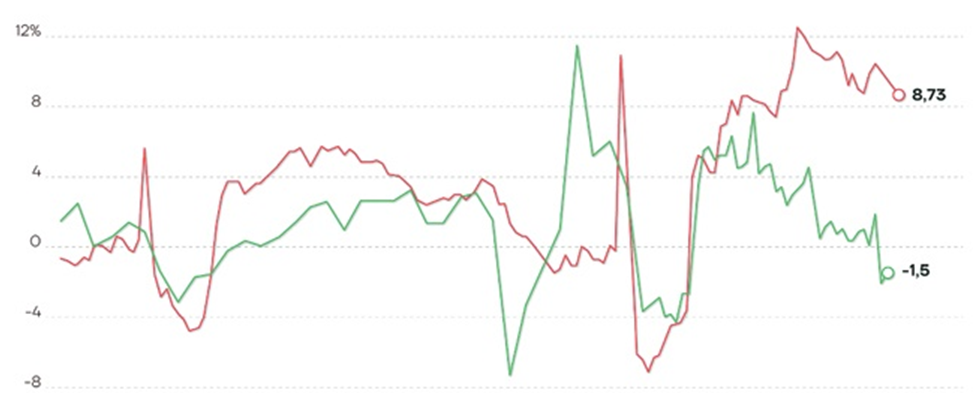

/ Central Bank real interest rate, %/ GDP growth, % year-on-year

| Feb 2014 | May 2015 | Aug 2016 | Nov 2017 | Feb 2019 | May 2020 | Aug 2021 | Nov 2022 | Feb 2024 | May 2025 |

A chart accompanying the report compares the dynamics of the Central Bank’s real interest rate and Russian GDP growth. Source: Roscongress

An interesting detail is that some experts have criticised the Russian Central Bank for following International Monetary Fund (IMF) prescriptions. Yet the Roscongress authors also cited IMF research in support of revising monetary policy, including a study published in spring 2026.

That IMF study examined the success of the ‘Asian tiger’ economies of South Korea, Japan, Singapore and Taiwan, which achieved rapid growth in the late twentieth and early twenty-first centuries.

‘They benefited from the creation of a leading state agency managing economic growth,’ the report authors wrote.

The Roscongress publication joins a growing list of similar reports issued by organisations such as the Centre for Macroeconomic Analysis and Short-Term Forecasting (CMASF) and the Institute of Economic Forecasting at the Russian Academy of Sciences.

CMASF has called for maintaining price stability as the priority of monetary policy while amending legislation to require consideration of economic growth as well (see Nezavisimaya Gazeta, May 6, 2026). Its analysts also argued that the Bank of Russia and the government should pursue coordinated policies aimed at both price and economic stability.

Some of the legislative amendments proposed by CMASF appeared questionable, however, especially from the perspective of the flexibility sought by businesses and analysts.

One proposed amendment would insert the specific word ‘low’ into the Central Bank law in relation to inflation, a term that is currently absent.

The Bank would thus be required to maintain ‘low and stable inflation’ while also taking economic growth into account. Critics noted that such wording would create interpretive difficulties, since it would raise the question of what level of inflation should be considered ‘low’.

Even so, despite some rough edges, the analytical note appears not to have gone unnoticed by either the government or the presidential administration. Discussion of the Central Bank’s mandate has moved to an entirely different level. What was once confined to informal conversations during conference coffee breaks has become a high-profile policy initiative taken seriously by officials.

The Institute of Economic Forecasting of the Russian Academy of Sciences has likewise argued that ‘a regime must be built in which fiscal, macroprudential, sectoral and monetary measures work in coordination rather than in opposition’. Otherwise, it warned, the country risks a ‘systemic crisis’ (see Nezavisimaya Gazeta, May 24, 2026).

ORIGINAL: NG/Russia’s Inflation Policy ‘Should Be Decoupled’ From the War Effort