Russia’s microcredit market has undergone several transformations. Amid tighter regulation, microfinance organisations (MFOs) have seen an influx of customers rejected by banks. These are not marginal borrowers but relatively reliable clients who need financing not merely to bridge the gap until payday but to make major purchases or keep a business afloat. As a result, MFO portfolios are increasingly dominated by longer-term loans resembling bank credit, as well as credit lines that function much like bank credit cards.

At the same time, MFOs have become increasingly selective in building their own base of trusted clients, rejecting as many as 80% of first-time loan applications. However, this alternative lending market now risks stalling, potentially driving some borrowers towards illegal and shadow lenders.

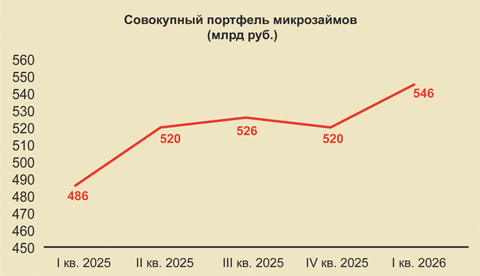

At the end of the first quarter, the total microloan portfolio stood at around RUB 546 bln, up nearly 5% over the quarter, while new lending declined by about 6% to RUB 357 bln.

These dry figures, showing one indicator rising while another falls, vividly illustrate the transformation of Russia’s microfinance sector. It is becoming increasingly inaccurate to describe it simply as a market for quick loans or payday lending.

Portfolio growth despite declining issuance was driven by a shift towards longer-term loans that increasingly resemble bank credit products.

That is according to a new report by the self-regulatory organisation MiR, which unites leading participants in Russia’s microfinance industry and represents more than 80% of the market.

As Andrei Ponomarev, chief executive of the Webbankir platform, explained to Nezavisimaya Gazeta, payday loans are typically issued for up to 30 days, with an average size of RUB 10,000–12,000 and are generally repaid in a single payment.

However, this type of lending is increasingly being displaced by longer-term products with maturities of up to a year or more, and in some cases up to five years. The typical maximum loan amount is around RUB 100,000, although higher limits are available depending on an MFO’s policy, the borrower’s credit history and repayment capacity. Unlike payday loans, these products are repaid through regular monthly instalments.

Nezavisimaya Gazeta found that at some microfinance providers, loans with maturities longer than traditional payday products now account for between 50% and, in some cases, as much as 90% of the portfolio.

Much of the demand for these longer-term loans comes from customers rejected by banks. Such borrowers are already familiar with conventional lending products, and MFOs attract them through more flexible credit-scoring systems than those used by banks.

It should also be noted that almost half of all MFO lending, 47.5% of the portfolio, is accounted for by captive MFOs directly affiliated with banks. In other words, banks themselves have helped channel customers into their own affiliated microfinance businesses.

According to Artem Pavlov, commercial director at Lime Credit Group, these ‘post-bank borrowers’ generally have more stable finances, are willing to plan over the long term, hold formal employment, have verifiable income, maintain good credit histories and are prepared to provide more extensive documentation.

According to Alfa-Dengi, borrowers typically use these longer-term MFO loans to purchase consumer electronics, finance home repairs, pay for medical treatment or education, or cover temporary cash-flow gaps.

Yulia Ledeneva, business development director at Joy Money, confirmed that such products are particularly popular among self-employed workers when they need to bridge short-term cash-flow shortages related to the purchase of equipment or consumable materials.

Another transformation is the growing popularity of credit lines within the MFO sector. ‘They allow a customer to receive a personal borrowing limit once and then access funds instantly whenever needed without repeatedly submitting applications, undergoing checks or waiting for approval. The mechanism is similar to a bank credit card,’ said Artem Bykov, chief executive of Moneyman.

A third shift is that, although MFOs continue to use more flexible credit-scoring models than banks, they are increasingly focused on building a base of trusted repeat customers while screening out less desirable applicants.

According to MiR statistics, rejection rates for first-time applications now stand at around 80%, broadly in line with trends in the banking sector. By contrast, rejection rates for repeat borrowers are only about 17%.

This reflects both tighter regulation affecting the MFO sector and simple business logic. ‘The marketing costs of retaining loyal customers are several times lower than the costs of attracting new ones,’ Ponomarev explained.

Yet just as this alternative lending market had begun to establish itself in forms previously uncharacteristic of the sector, it found itself facing another transformation, one that could prove painful for all participants.

In its latest report, MiR warned of a high risk that customers will increasingly turn to illegal lenders once biometric identification requirements are extended to the entire online microfinance market.

Since March 1 this year, some MFOs have been required to issue online loans only to borrowers whose biometric data are registered. This requires a digital scan of both a customer’s face and voice. The measure is intended to prevent fraudsters from manipulating citizens into taking out microloans.

In 2026 the requirement applies only to microfinance companies (MFCs), a subtype of MFO authorised to issue loans of up to RUB 1 mlnto individuals and to issue bonds.

Total microloan portfolio (RUB bln)

Total microfinance sector portfolio grew significantly during the quarter. Source: MiR self-regulatory organisation.

The consequences of the new rule are already becoming apparent. ‘The requirement has led most MFCs, which account for around 20% of loan issuance, to change their status to MCCs (microcredit companies, Nezavisimaya Gazeta) in order to avoid losing customer traffic, abandoning retail funding and bond issuance,’ MiR experts said.

From March 1, 2027, the biometric requirement will be extended to the entire microfinance sector, including MCCs, which are limited to issuing loans of up to RUB 500,000 to individuals.

Industry representatives warn that the current database of biometric profiles remains extremely limited. As a result, once the requirement is applied across the sector, the overwhelming majority of customers could effectively be cut off from MFO services.

Technically, the requirement applies only to online lending, which would appear to leave an obvious solution: directing borrowers to physical offices

‘Some companies may experiment with office-based lending, but this is unlikely to generate any meaningful increase in business because, under their existing operating models, issuing loans without biometrics in physical branches is not feasible for the overwhelming majority of firms,’ MiR said.

Moreover, surveys indicate that MFO customers overwhelmingly prefer remote channels, valuing the convenience and speed of obtaining loans without visiting an office.

Alexei Rodin, founder of Rodin.Capital, explained why a return to branch-based lending would be difficult. Over recent years the sector has moved heavily online in response to customer demand. As a result, maintaining branch networks became uneconomic, while rebuilding them would require substantial investment.

Maintaining a single office in a small town can cost between RUB 2 and 5 mln (per month, Nezavisimaya Gazeta). To provide adequate coverage, offices would need to be located in every district. Even modest banks typically operate between 30 and 50 branches. Multiply those figures by even the most conservative estimates of operating costs and annual investment requirements reach between RUB 1 and 3 bln,’ Rodin said.

For this reason, industry participants conclude that if borrowers rejected by banks are also unable to obtain financing from MFOs, whether online or in person, many will inevitably turn to illegal lenders operating in the shadow economy.

Illegal lenders are individuals or organisations that operate without a licence and outside the Bank of Russia’s register, meaning outside the framework of applicable financial legislation,’ MiR’s press service told Nezavisimaya Gazeta. ‘Unfortunately, it is difficult to estimate precisely how many Russians are at risk, but various assessments suggest the figure could run into several million people.’

As a result, the industry is now focusing considerable effort on improving financial literacy and informing customers about the upcoming biometric requirements.

ORIGINAL:NG/Borrowers Without Biometrics May Soon Have Nowhere Left to Borrow Legally